The global shipping sector is at a pivotal moment. With the IMO’s net-zero target for 2050 and the EU Green Deal aiming for climate neutrality, decarbonising maritime transport is urgent. Hydrogen derivatives or electro fuels such as ammonia, methanol, and renewable hydrogen offer a promising pathway, though production, distribution, and port infrastructure readiness remain uneven.

The Interreg Baltic Sea Region project, H2Deri@BSP conducted a comprehensive market analysis across eight countries and partner ports in the Baltic Sea Region. By combining literature research with surveys, interviews, and workshops, the project partner IVL Swedish Environmental Research Institute mapped nearly 300 hydrogen-related initiatives, examining demand, production capacities, infrastructure readiness, regulations, and import-export potential. Many initiatives are still in planning, but the study provides a clear view of the region’s hydrogen landscape.

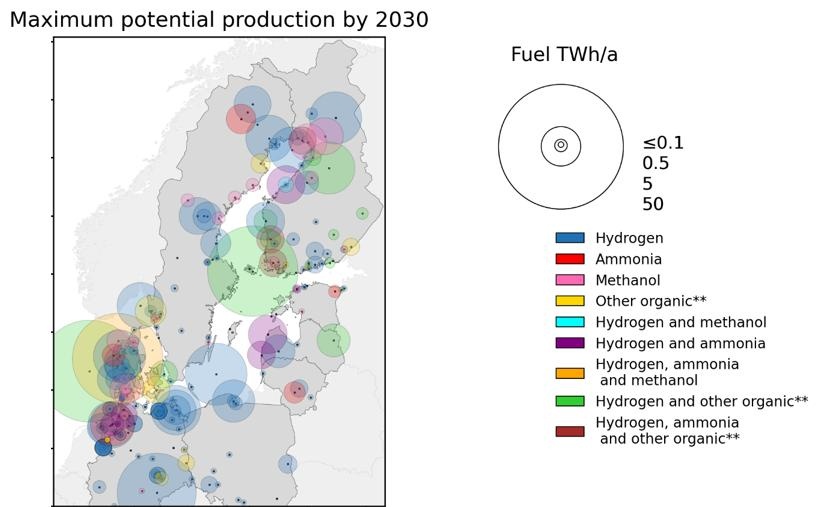

If planned projects are realised, hydrogen-derived energy production could reach 338 TWh by 2030, equivalent to 31 million tonnes of Marine Gas Oil. While Denmark and Finland are targeting export of hydrogen and its derivatives, Germany is developing import corridors and focused on port conversions. Sweden emphasizes on industrial and maritime hydrogen, while Poland along with the Baltic States show promising hydrogen valley initiatives.

Findings show the Baltic Sea Region is gaining momentum in renewable maritime fuels, yet hydrogen derivatives are in early stages. EU regulations such as FuelEU Maritime, AFIR, and the EU Emissions Trading System are shaping the market, though fragmented policies and slow national implementation limit large-scale deployment.